Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

For many Americans, preparing for retirement is a delicate balance between investment performance, tax benefits and anticipating future needs.

Retirement accounts such as Individual Retirement Accounts (IRAs) play a central role in this equation.

But for high-income taxpayers, direct access to certain tax advantages, such as those offered by Roth IRAs, is restricted. This is where a little-known but powerful strategy comes into play: the Backdoor IRA.

The Backdoor Roth IRA is not a special account, but a tax strategy. It allows people whose income exceeds the IRS thresholds to indirectly access a Roth IRA.

It involves contributing after-tax money to a Traditional IRA (a non-deductible contribution), then converting these funds into a Roth IRA.

This allows you to benefit from the advantages of the Roth, in particular growth and tax-free withdrawals at retirement, while bypassing income limits.

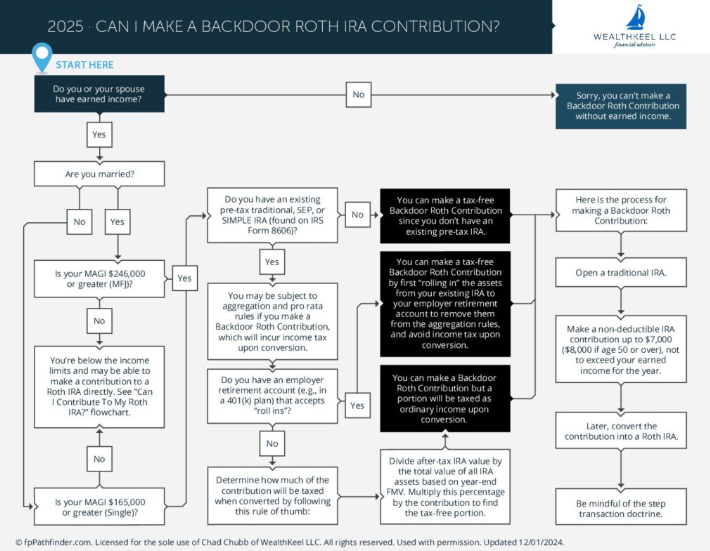

In 2025, single taxpayers can no longer contribute directly to a Roth IRA if their Modified Adjusted Gross Income (MAGI) exceeds $165,000. For married couples filing jointly, the limit is $246,000, according to the IRS requirements. These thresholds effectively exclude many executives, entrepreneurs and professionals.

Through the “back door”, these taxpayers can still invest up to $7,000 a year ($8,000 if age 50 or over) in a Roth IRA. And there are no income restrictions. A rare opportunity to optimize your retirement planning strategy over the long term.

There are four key steps to implementing this strategy:

It is essential not to invest the funds prior to conversion, and to comply with all tax formalities, otherwise the tax authorities may wrongly consider the entire conversion to be taxable.

One of the main pitfalls of the Backdoor IRA is the famous “pro-rata rule”. This rule requires that all of a taxpayer’s Traditional IRAs (including SEP and SIMPLE IRAs) be taken into account when determining the taxable portion of the conversion.

For example, if you already have $90,000 in pre-taxed Traditional IRAs, and you add $10,000 in non-deductible contributions, any conversion will be considered to contain 90% taxable funds. This can result in an unexpected tax bill.

Fortunately, there are ways around this rule, including transferring old IRAs to a company 401(k), which doesn’t enter into the pro-rata calculation.

The Roth IRA offers unique retirement benefits:

In other words, this strategy allows you to optimize your tax situation at retirement, protect your future income and even organize your succession with a Roth IRA.

This strategy is particularly relevant if:

But beware, this is not a one-size-fits-all solution. If you need the funds in the short term, or if you don’t want to deal with the tax complexities associated with the pro-rata rule, it’s best to consult a tax advisor before taking the plunge.

Against a backdrop of increasing tax pressure and uncertainty about the future of Social Security, every opportunity to optimize your retirement tax situation counts.

The Backdoor IRA is one such powerful strategy that, although technical, can offer lasting benefits to high-income households concerned about their future financial independence.

However, it’s important to master the rules, and not to overlook the importance of professional guidance, as one misstep can be costly. But if properly executed, this strategy can make the difference between a tax-free retirement… and a taxed retirement.

An IRA (Individual Retirement Account) allows you to make tax-deferred investments to save money and provide financial security when you retire. There are different types of IRAs, the most common being a traditional one – in which contributions may be tax-deductible – and a Roth IRA, a personal savings plan where contributions are not tax deductible but earnings and withdrawals may be tax-free. When you add money to your IRA, this can be invested in a wide range of financial products, usually a portfolio based on bonds, stocks and mutual funds.

Yes. For conventional IRAs, one can get exposure to Gold by investing in Gold-focused securities, such as ETFs. In the case of a self-directed IRA (SDIRA), which offers the possibility of investing in alternative assets, Gold and precious metals are available. In such cases, the investment is based on holding physical Gold (or any other precious metals like Silver, Platinum or Palladium). When investing in a Gold IRA, you don’t keep the physical metal, but a custodian entity does.

They are different products, both designed to help individuals save for retirement. The 401(k) is sponsored by employers and is built by deducting contributions directly from the paycheck, which are usually matched by the employer. Decisions on investment are very limited. An IRA, meanwhile, is a plan that an individual opens with a financial institution and offers more investment options. Both systems are quite similar in terms of taxation as contributions are either made pre-tax or are tax-deductible. You don’t have to choose one or the other: even if you have a 401(k) plan, you may be able to put extra money aside in an IRA

The US Internal Revenue Service (IRS) doesn’t specifically give any requirements regarding minimum contributions to start and deposit in an IRA (it does, however, for conversions and withdrawals). Still, some brokers may require a minimum amount depending on the funds you would like to invest in. On the other hand, the IRS establishes a maximum amount that an individual can contribute to their IRA each year.

Investment volatility is an inherent risk to any portfolio, including an IRA. The more traditional IRAs – based on a portfolio made of stocks, bonds, or mutual funds – is subject to market fluctuations and can lead to potential losses over time. Having said that, IRAs are long-term investments (even over decades), and markets tend to rise beyond short-term corrections. Still, every investor should consider their risk tolerance and choose a portfolio that suits it. Stocks tend to be more volatile than bonds, and assets available in certain self-directed IRAs, such as precious metals or cryptocurrencies, can face extremely high volatility. Diversifying your IRA investments across asset classes, sectors and geographic regions is one way to protect it against market fluctuations that could threaten its health.