Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Meta just posted an impressive Q2 2025 earnings report, sending shares soaring over 11% in pre-market trading. Revenue jumped 22% YoY to $47.5 billion, with EPS hitting $7.14 — a 38% increase over Q2 2024. But beyond the headline numbers, a deeper story is unfolding.

While most investors were focused on topline growth and AI infrastructure spending, Meta quietly revealed something far more material: GenAI is no longer just hype. It’s delivering hard ROI in the ad business.

Perhaps the most underappreciated — and yet most consequential — detail from Meta’s earnings was the 5% uplift in ad conversions on Instagram and 3% on Facebook attributed directly to its new GenAI-powered ad ranking systems. That’s the first concrete, measurable proof of GenAI’s effectiveness in Meta’s core business.

The Street had been pricing GenAI as a long-term story. But with conversion lift now quantifiable, analysts will likely begin revising their ad ARM (average revenue per mille) models upward. This could prompt not just EPS upgrades, but a multiple re-rating if investors start to price in compounding returns from AI-enabled ad performance.

Yet oddly, Meta’s management didn’t highlight this in the press release or even in their opening remarks. It was buried in the call — a potential oversight that sharp investors won’t ignore for long.

CFO Susan Li also signalled another sharp increase in AI infrastructure CapEx in 2026, when the Street had been modelling a plateau. This isn’t just about spending — it’s a forward-looking signal. Meta expects strong ROI on its infrastructure bets, particularly in reducing latency, improving model throughput, and enabling more scalable GenAI products.

The implication? If early signs of infrastructure yield (like faster ad delivery or improved AI engagement) start to show up in metrics, investors could get another leg higher on the stock. But it’s something to watch closely — forward unlocks like this can be fragile if they don’t materialise quickly.

That said, not everything is bullish. Meta may be downplaying a major Q3 revenue risk tied to the EU’s Digital Markets Act (DMA). The company’s Less Personalised Ads (LPA) model — designed to comply with EU privacy guidelines — is under fresh scrutiny. If the European Commission enforces new rules mid-quarter, Meta’s ad revenue from the EU could take a hit, and this risk is not yet modelled in consensus estimates.

As such, any sign of regulatory pressure in August or early September could be a sell trigger — especially if accompanied by weakness in European engagement metrics.

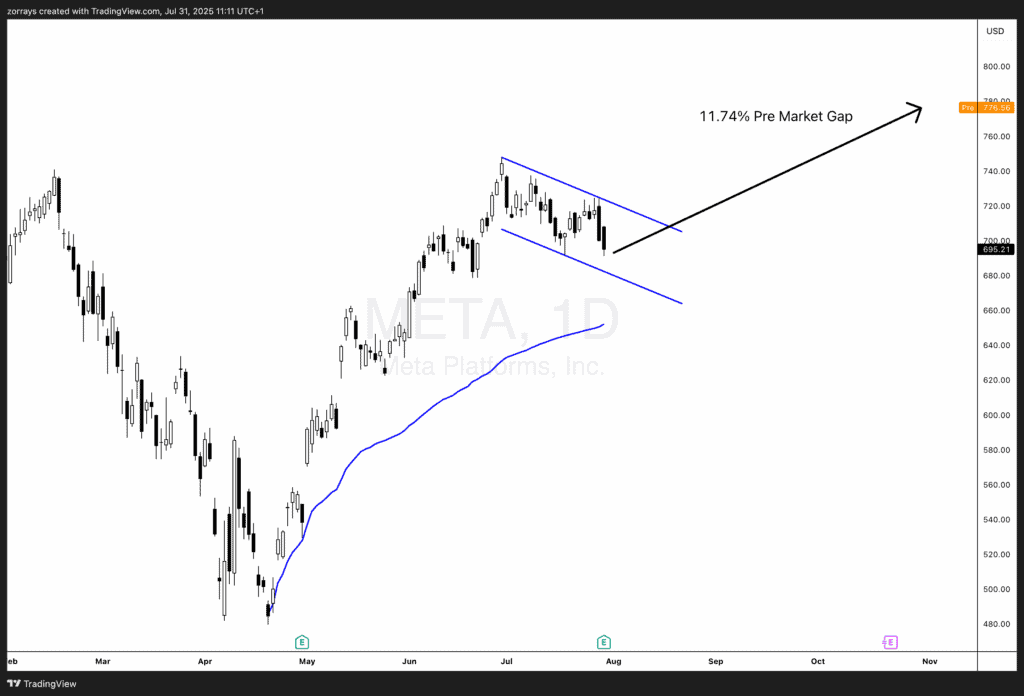

From a technical standpoint, Meta’s stock had been consolidating within a bullish flag pattern, suggesting potential for a breakout whilst hovering above the Anchored VWAP. With the strong earnings, the 11.74% pre-market gap up confirms that breakout is in play.

But as we’ve seen, this isn’t a clean technical narrative. Despite the breakout, it’s hard to ignore the overhang of regulatory uncertainty in Europe. As retail traders jump in on the bullish momentum, the smart money may remain cautious — or even fade the move — if EU risk crystallises.

Meta is now transitioning from GenAI hype to GenAI execution. The ad conversion numbers are real. The infrastructure investments are deliberate. And the stock is reacting accordingly.

But don’t ignore the storm clouds. Regulatory pressure in the EU and unmodeled downside risks could undercut the bullish narrative quickly.

For now, the trend is your friend — but stay alert. Meta’s story is still being written, and the next chapter may hinge as much on Brussels as it does on Menlo Park.